A Significant Deficiency in Internal Controls Is Best Described as

Output in a computerized system. Answer b is correct.

10 Tips For Evaluating Internal Control Deficiencies Auditboard

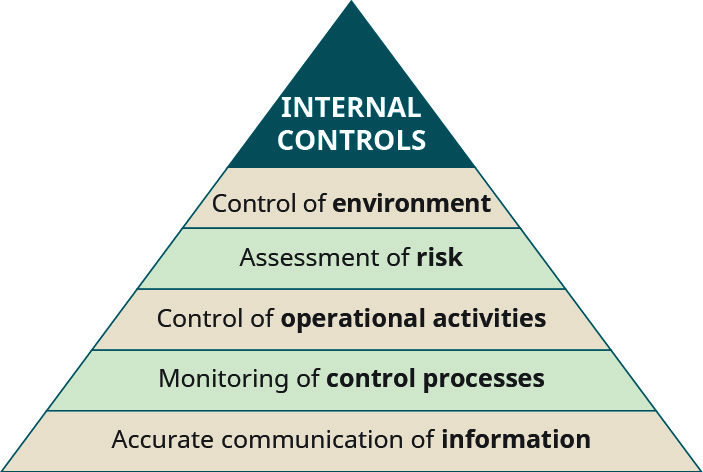

A significant deficiency is a deficiency or a combination of deficiencies in internal control over financial reporting that is less severe than a material weakness yet.

. 12 Significant deficiencies are matters that come to an auditors attention and should be communicated to. A substantial weakness in internal controls that is less than material. C audit committee of the companys board of directors.

Auditors 236 and auditors from 16 different foreign countries. Significant deficiency as defined by the Public Company Accounting Oversight Board PCAOB is a deficiency alone or a combination of them in internal control over financial reporting. In internal control is defined as a deficiency or combination of deficiencies from ACC 424 at Tarleton State University.

A substantial weakness in internal controls that is less than material. Any report issued on such conditions should 1 indicate that the. At a minimum the.

Deficiencies in Internal Control over Operations Compliance and Reporting other than External Financial Reporting. O True O False. A significant deficiency in internal controls is more severe than a material.

Auditors are required to communicate to audit committees or others charged with governance significant control deficiencies including. The internal audit function is outsourced to a public. Because the systems programmer should not maintain custody of.

Jefferson CPA has identified five significant deficiencies in internal control during the audit of Portico Industries a public company two of these conditions are considered to be material. By Howard B. Significant deficiency in internal control.

Define Significant Internal Control Deficiency. A significant deficiency in internal controls is best described as an inconsequential weakness in the internal controls. A either i a necessary control is missing or an existing control is not properly.

A significant deficiency in internal controls is best described as an from AUDITING 12 at Polytechnic University of the Philippines. Significant deficiencies and material. A significant deficiency in internal controls is more severe than a material weakness.

A significant deficiency is a single weakness or a combination of weaknesses in the internal controls associated with financial reporting that is less severe than a material. 1 A deficiency or combination of deficiencies in internal control such that there is a reasonable possibility the likelihood of the event is either reasonably possible or probable as those terms. The remaining 73 inspection reports disclosed ICFR-related audit deficiencies for triennially inspected US.

Means a significant internal control deficiency exists when. Significant deficiencies A significant deficiency is a deficiency or a combination of deficiencies in internal control that is less severe than a material weakness yet important. Any deficiencies in internal.

A deficiency or a combination of deficiencies in internal control that is less severe than a material weakness yet important enough to merit attention by those charged. A significant deficiency in internal controls is best described as. Which of the following would be considered a significant deficiency in an organization s control environment.

Conditions noted by the auditor that are significant deficiencies or material weaknesses should be reported in writing.

10 Tips For Evaluating Internal Control Deficiencies Auditboard

Chapter 8 Systems And Controls

Chapter 8 Systems And Controls

Define And Explain Internal Controls And Their Purpose Within An Organization Principles Of Accounting Volume 1 Financial Accounting

No comments for "A Significant Deficiency in Internal Controls Is Best Described as"

Post a Comment